The previous year was tough on all of us, but let’s hope those tough times stay away! Those times provided many challenges to us and our families and many people were hit with financial challenges that impacted them in new ways. On the other hand, the stock market performed incredibly well and the savings rate in the U.S. skyrocketed during the pandemic. Many people saw their portfolio grow and grow and you most likely received many referrals for new clients.

Both are exciting! Also great to have included in your professional on-boarding process. Interviewing the client to understand their investment objectives and helping them clarify those objectives and then charting a path to help them get there. This is where trust is built; listening closely to what the new client says, and building a plan from there.

The Average Financial Advisor focuses on the Asset side of the balance sheet. How can we grow and protect the assets of this client and their family is the most important question you answer. That is why you are there, to provide this very important role in their lives.

Some Financial Advisors will discuss Estate Planning or explore tax issues the client may be facing. Others may even address insurance, i.e.) does the client have enough protection in their plan to deal with unforeseen events?

This is where the typical on-boarding process ends but there is a key aspect that is missing – the liability side of the balance sheet. What are their debts costing them and are they Borrowing Smart?

This analysis, as seen below, is how I start with my clients. The main reason to do this is to bring clarity to the cost of their borrowing. I call it my Borrow Smart Analysis. We did this analysis all the time in business school for a Corporation so the CFO could deploy their cash flow in the most efficient manner. Do they invest in the business or pay off debt?

How do they manage their cash flow? Why not do this for our clients?

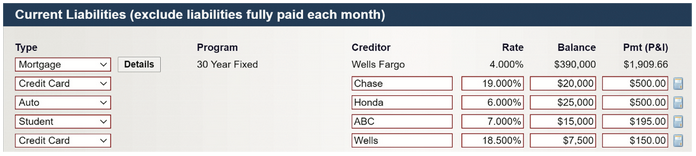

Let’s take a look at my case study. Here is where I enter their current debts:

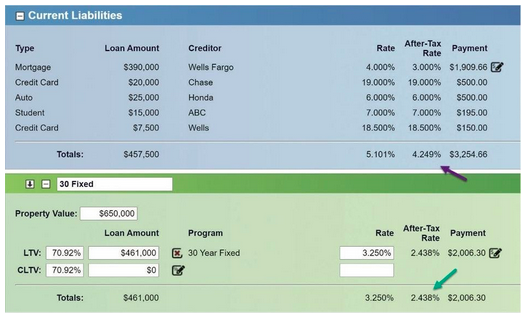

Then we see if there is an opportunity for them to lower their cost of capital and deploy their cash flow more efficiently:

If this client sees that they are currently borrowing at 4.249 percent after tax and can bring that down to 2.438 percent with a refinance of their mortgage, that accomplishes two things: 1. It lowers their cost of capital and 2. It increases their free cash flow. Two AWESOME improvements!

Now, from the perspective of the Financial Advisor, this also accomplishes two amazing things:

- The client has clarity on their cost of borrowing and it becomes very easy for them to understand that the highest and best use of their free cash flow is NOT paying down their mortgage – it is INVESTING and out running that very low cost of capital.

- Each month, they are able to invest more WITHOUT affecting what they have been experiencing on their current cash flow. In my example below the client can increase their monthly investing by over $1200 without a change in lifestyle!

This is the Power of Liability Management and how it can help your client protect and grow their assets.

I am here to help if you need it when on-boarding a new client or clarifying this concept for an existing client, just email me to set up a time to talk and we can help others get even more clarity on their personal financial world and managing their liabilities.