The housing market is a constantly changing landscape with new regulations, trends, and economic shifts. With the recent changes in mortgage rates, it’s important to understand how these factors can impact your future purchase or sale of a property.

How it affects home sellers and buyers?

For any potential buyers, changes in mortgage rates impact the purchasing power – when rates are lower, you can afford more home.

Chief Economist at First American, Mark Fleming, explains:

“Monthly payments have remained manageable despite soaring home prices because of low mortgage rates. In fact, monthly payments remain below the $1,250 to $1,260 range that we saw in both fall 2018 and spring 2019, but they are on track to hit that level this spring. Although they remain low, mortgage rates have begun to increase and are expected to rise further later in the year, thus affordability will test buyer demand in the months ahead and likely help slow the pace of price growth.”

Industry professionals suggest entering the market sooner rather than later can help you reap the most benefits in homeownership.

For sellers, it is your market. Due to the low inventory available, buyers are hopping on the opportunity to secure a low rate and find a home fast. Sellers are receiving multiple offers on their home and the competition is strong, giving sellers leverage with negotiations.

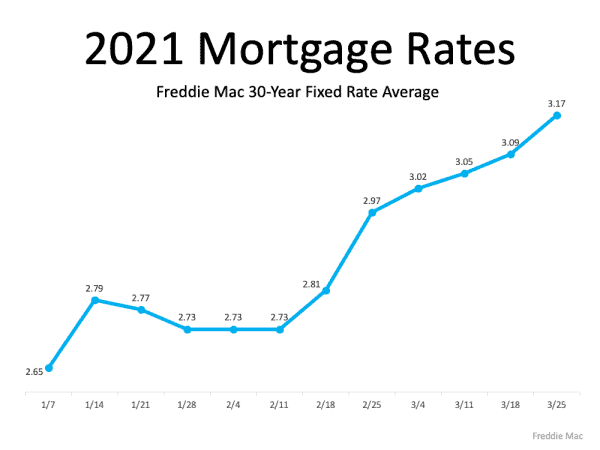

Will interest rates come down or rise again?

Federal Reserve Chairman, Jerome Powell, made it clear that the Fed will not be raising interest rates any time soon. We might not see any significant rise until 2023. Rates decreased to keep a healthy economy and stimulate spending through cheaper borrowing costs for consumers, borrowers, and businesses alike. However, as we’ve seen already in 2021 when these changes take effect on mortgage interest rates, there may be some implications on prices as well as who can qualify for a home loan.

Does it impact inventory to purchase from builders or from existing?

The National Association of Realtors (NAR) responded to the recent jobs report and stated that construction jobs saw one of the biggest gains ever in March with 110,000 new additions. The Chief Economist at NAHB, Robert Dietz states: “Good job numbers in March for residential construction. 37,000 gain from Feb to March. 3.03 million total employment for home builders and remodelers, and up 49,100 from Jan 2020.” This is good news because of the potential home building inventory that can become available in the market. More available homes may also keep home prices to affordable levels for many potential homebuyers.

The jobs report from The U.S. Bureau of Labor did state the unemployment was down 6 percent in March. With the growth in construction jobs and hope for decreasing unemployment numbers, experts are expecting an increase in available homes, and a positive economy, and a strong housing market for 2021.

A healing economy, inflation concern, and unemployment all play into the changes in rates and how they could impact your decision. It’s important to stay up to date on the latest changes. Reach out to us so we can work together on your real estate and mortgage goals this year.

This article is intended to be accurate, but the information is not guaranteed. Please reach out to us directly if you have any specific real estate or mortgage questions or would like help from a local professional. The article was written by Sparkling Marketing, Inc. with information from resources like Freddie Mac, NAR, and NAHB.